Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Forbes.com – Declining mortgage rates—it’s the holiday gift that keeps on giving.

Since hitting a 2023 high in late October, the average 30-year fixed receded below 7% in mid-December for the first time in four months.

The average 30-year fixed rate slid another 28 basis points this week to 6.67%, the eighth consecutive week of decreases, according to Freddie Mac. A basis point is one-hundredth of one percentage point.

Yet, despite this easing, a perfect storm of still-high mortgage rates and home prices amid historically low housing stock continues to put homeownership out of reach for many—most notably first-time buyers—who remain more pessimistic than ever about being able to afford a home as we close in on 2024.

2023 was a demoralizing year for many aspiring home buyers.

Mortgage rates surged—hitting a high of 7.79%—and median home prices in the third quarter were north of $400,000. Moreover, in July, average monthly payments hit their highest level ever at $2,306, according to Intercontinental Exchange, a financial technology and data services provider.

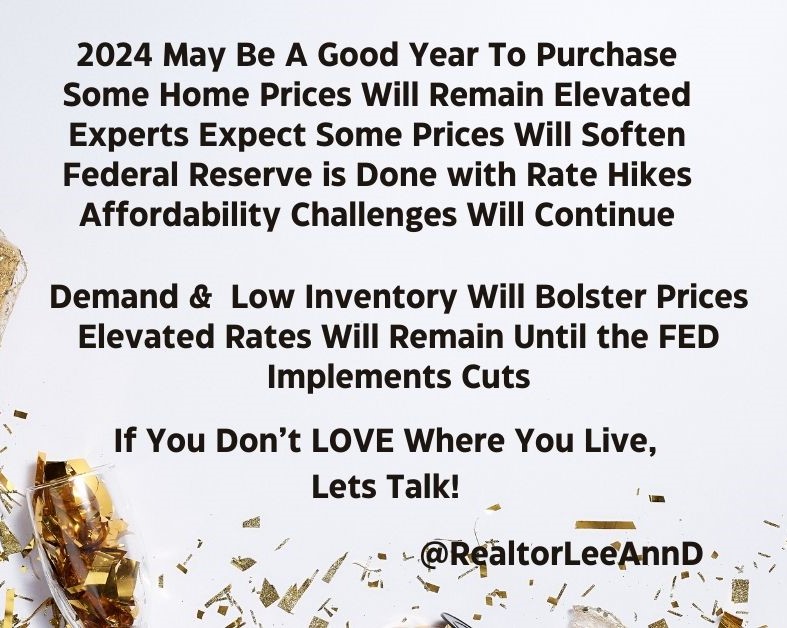

However, 2024 may be a better year to purchase a home—at least for some. While home prices will likely remain elevated—and even increase in some markets—industry experts expect prices in certain areas of the country to soften.

Economists are also optimistic that the Federal Reserve is done with its rate-hiking campaign to lower inflation after policymakers kept the federal funds rate unchanged for a third straight meeting on December 13. The federal funds rate is the benchmark interest rate financial institutions charge each other for overnight loans; it tends to indirectly influence mortgage rates.

Even so, affordability challenges will continue in 2024. Pent-up demand and low inventory will generally bolster prices, and elevated mortgage rates will remain until the Fed implements cuts to the federal funds rate.

Mark Fleming, chief economist at First American Financial Corporation, predicts a “flat stretch” ahead for the housing market. “If the 2020-2021 housing market was too hot, then the 2023 market was probably too cold, but 2024 won’t yet be just right,” Fleming said in his 2024 forecast.

For a housing recovery to occur, Gumbinger says several conditions must unfold.

“For the best possible outcome, we’d first need to see inventories of homes for sale turn considerably higher,” Gumbinger says. “This additional inventory, in turn, would ease the upward pressure on home prices, leveling them off or perhaps helping them to settle back somewhat from peak or near-peak levels.”

And, of course, interest rates would need to cool off.

But Gumbinger says don’t hope they cool too quickly. Rapidly falling rates could create a surge of demand that wipes away any inventory gains, causing home prices to rebound.

“Better that rate reductions happen at a metered pace, incrementally improving buyer opportunities over a stretch of time, rather than all at once,” Gumbinger says.

He adds that mortgage rates returning to a more “normal” upper 4% to lower 5% range would also help the housing market, over time, return to 2014-2019 levels. Yet, Gumbinger predicts it could be a while before we return to those rates.

Source: https://www.forbes.com/advisor/mortgages/real-estate/housing-market-predictions/